The Economics of Generative AI

🌈 Abstract

The article discusses the economics of Generative AI, analyzing where value and profits have accrued so far, and where they are likely to shift in the future.

🙋 Q&A

[01] Where has value accrued in Gen AI so far?

1. Questions related to the content of the section?

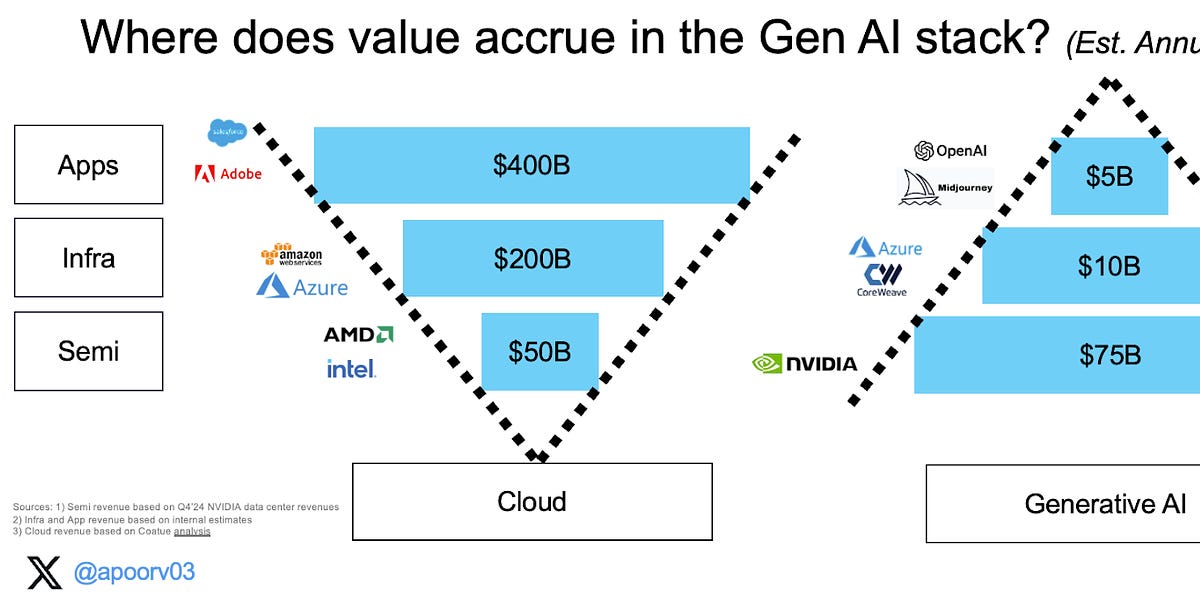

- The Gen AI stack today is A-shaped, unlike the V-shaped cloud stack, with the semiconductor (semi) layer capturing the majority of the value.

- The semi layer (primarily NVIDIA) accounts for ~83% ($75B out of $90B) of the total Gen AI revenues today.

- In contrast, the application layer accounts for only ~$5B in revenues, while the infrastructure (infra) layer accounts for ~$10B.

[02] Where have profits accrued in Gen AI so far?

1. Questions related to the content of the section?

- The profitability of the Gen AI stack is also inverted, with the semi layer capturing ~88% of the total gross profits ($64B out of $73B).

- The application layer is estimated to have ~50-55% gross margins, the infra layer ~65% (without depreciation) or 25-30% (with depreciation), while the semi layer (NVIDIA) has upwards of ~85% gross margins.

[03] Where do we go from here?

1. Questions related to the content of the section?

- The author expects the current structure of Gen AI revenues (inverted pyramid) to change over time, with the application layer capturing a higher proportion of the value chain.

- This transition is expected to follow a similar pattern as seen in the mobile and cloud computing waves, where value initially accrued in the hardware layer before shifting to the software/application layer.

- The author identifies several critical questions that will shape this transition, such as:

- Will NVIDIA's high margins be sustainable?

- How will the profitability of AI applications improve over time?

- How will the value shift in the consumer Gen AI market?

2. How does the author expect the value distribution to evolve in the Gen AI ecosystem? The author expects the value in the Gen AI ecosystem to shift from the semiconductor layer to the application layer over time, following a similar pattern as seen in the mobile and cloud computing waves. Initially, the hardware (semiconductor) layer captured the majority of the value, but over time, the value shifted towards the software/application layer.